In March 2025, a class action lawsuit was filed in Duval County Circuit Court against LVL Living, a prominent multi-state property management company operating rental housing throughout Florida. The case—Joyner, et al v. LVL Living LLC, et al, Case No. 16-2025-CA-001265 (Duval County)—raises serious allegations concerning LVL Living’s tenant billing and deposit practices and has drawn attention across the residential landlord-tenant industry. This is not the only significant class action lawsuit with significant impact on the landlord business. The largest landlord in the United States, Greystar, is also facing a class action lawsuit. There are many risks inherent in the landlord business, and this case highlights the risk of not following “best practices”.

Introduction: The $34K Lawsuit Rocking FL Landlords

The Tenant-Plaintiffs, representing a putative class of former tenants, allege that the Landlord-Defendants (LVL Living) engaged in a systematic practice of unlawfully retaining security deposits, assessing unauthorized or illegal fees, and failing to comply with Florida’s statutory notice and refund requirements. They further contend that these actions were not isolated events but rather part of a uniform policy applied across all LVL-managed properties, potentially affecting hundreds or thousands of renters.

The complaint also asserts claims for breach of contract, unjust enrichment, and violations of the Florida Deceptive and Unfair Trade Practices Act (FDUTPA)—suggesting that LVL’s practices constituted a deliberate pattern of overcharging tenants and circumventing both lease terms and state law protections.

As this lawsuit progresses, it could have wide-ranging implications not only for LVL Living but also for landlords and property managers across Florida. This article provides a comprehensive review of the allegations, legal theories, and procedural posture of the case—and explores what it may mean for the future practices in Florida’s rental housing market.

Case Breakdown: LVL Living’s Alleged Violations

The Plaintiffs, acting on behalf of themselves and a proposed class of similarly situated tenants, allege that:

- LVL Living operates multiple rental properties across Florida, including in Jacksonville (Duval County), and manages these properties through a centralized system.

- Plaintiffs were tenants at LVL Living-managed properties during the relevant period.

- The core factual allegation is that LVL Living systematically charged tenants unlawful and excessive fees and violated various Florida statutes, including the Residential Landlord-Tenant Act, Consumer Protection Act, and Deceptive and Unfair Trade Practices Act.

Plaintiffs seek:

- Certification of the case as a class action.

- Actual damages and statutory penalties.

- Disgorgement of wrongfully obtained funds.

- Attorney’s fees and costs.

- Injunctive relief prohibiting further unlawful practices.

Among the core allegations in the lawsuit are the Plaintiffs’ claims of extreme emotional and financial distress stemming from LVL Living’s post-tenancy debt collection practices.

According to the complaint, the Plaintiffs acknowledged falling behind on rent and understood they owed a delinquent balance of approximately $4,599.77, reflecting 2 months’ unpaid rent. However, their expectations were upended when they received a collection notice demanding not just past-due rent, but the entire remaining balance of their lease term—totaling over $34,000—with threats that the amount would escalate further within days.

The Plaintiffs allege that the situation was made worse when LVL Living transferred the claimed debt to a third-party debt collection company. These allegations form the factual basis for claims not only of improper accounting and billing practices, but also of potential statutory violations relating to debt collection and deceptive trade practices.

The $34K Demand: How Landlords Miscalculated

Here’s a chart to demonstrate how the landlord reached the total demand of over $34,000, which was sent to collections. This was taken from the Landlord’s security deposit claim notice, which was attached as an exhibit to the Plaintiffs’ complaint.

| Money Item | Amount |

| “Previous rents” (presumably this includes the $4,599.77 plus late fees on those 2 months’ rent, which the tenant does not dispute owing) | $5,640.11 |

| Concession Payback | $2,050.00 |

| Rent for remaining term of the lease | $17,032.00 |

| Final cleaning | $260.00 |

| Final admin | $20.00 |

| Subtotal | $25.002.11 |

| 40% collection fee | $10,000.84 |

| Security Deposit (credit) | -$250.00 |

Analyzing the Legality of the Landlord’s Post-Tenancy Money Claims

The Plaintiffs’ allegations raise important questions about whether LVL Living’s actions—claiming the full lease balance and additional charges from the security deposit and referring a $35,000 debt to a collection agency—complied with Florida law. While landlords are generally entitled to recover unpaid rent and certain damages under a lease, Florida law places limitations on the procedures landlords must follow when making claims against security deposits and when pursuing damages after a tenant vacates early or is evicted.

The following section examines whether LVL’s handling of the deposit and the subsequent referral of the alleged debt to a third-party debt collector aligns with these statutory requirements—and whether it may expose the landlord to liability for overreaching or deceptive practices, as well as some tips to help landlords avoid a tenant’s lawsuit of this kind.

Turning to the Lease: Was There a Contractual Basis for the Charges?

To determine whether LVL Living had the legal right to demand over $34,000 from the Plaintiffs following their eviction, it is necessary to examine the terms of the lease agreement itself. Under Florida law, a landlord’s ability to impose financial obligations beyond statutory defaults—such as accelerated rent, liquidated damages, or specific penalty fees—must be, at a minimum, grounded in clear, enforceable language within the lease. Without express contractual provisions authorizing such charges, a landlord’s attempt to collect them may be legally unsupported and potentially deemed a violation of consumer protection and debt collection statutes.

Back Rent

The Plaintiffs do not dispute that they owed a balance of $4,599.77 in unpaid rent at the time they vacated the property. That portion of the landlord’s claim appears to be valid and contractually supported, and it forms the uncontested foundation of the total amount pursued. The dispute, however, centers on the additional charges beyond the uncontested unpaid rent—particularly the demand for the full remaining lease balance, rent concession claw-back, and debt collection fee—which the Plaintiffs allege were excessive and improperly pursued.

Rent Concession Payback

In addition to unpaid rent, the landlord included a Rent Concession Payback charge. Rent concession claw-back addendum are commonly used in residential apartment leases to attract tenant pool and incentivize lease fulfillment.

This charge appears to stem from a lease provision or addendum allowing the landlord to retroactively revoke any rent discounts or concessions if the tenant defaulted before completing the lease term, but the lease agreement attached as an exhibit to the Plaintiff’s complaint does not contain a Rent Concession Addendum.

If there was no such Rent Concession addendum signed by the tenants, this could pose a significant problem for the Landlord, because that is necessary to provide the landlord with the right to charge that concession in the event the tenant does not fulfill the terms of their lease. If there was such an addendum that provided the landlord with that “claw-back” right, the terms of the addendum are likely vital to the outcome of this issue. The Plaintiff did not focus their lawsuit on the Concession charge, so that issue may not be litigated in this case.

Landlord Tip: Use a Clear Addendum for Rent Concession Claw-Backs

If you plan to offer rent concessions (e.g., move-in specials or discounted rent for the first few months) and want the ability to reclaim those concessions if a tenant breaks the lease early, it’s critical to document this clearly and separately:

- Use a written lease addendum that explicitly states:

- The amount and nature of the rent concession.

- That the concession is conditional upon the tenant completing the full lease term.

- That early termination or default will trigger repayment of the full concession amount.

- Ensure the language is specific and enforceable, not vague or punitive—courts may invalidate ambiguous clauses that resemble penalties rather than contractual conditions.

- Avoid applying claw-backs automatically without reviewing whether the tenant’s default actually justifies it (e.g., if the lease was nearly fulfilled or all rent was paid, enforcing a claw-back may not be equitable or enforceable).

By properly documenting rent concession terms and conditions, landlords can help protect their financial interests while minimizing legal exposure.

Acceleration Charge

One of the most contentious components of the landlord’s claim is the acceleration of all rent due under the remainder of the lease term ($17,032.00), which significantly increased the total balance sent to collections (consisting of $6,812.80 of the debt collection attempt). The Plaintiffs allege that, following their eviction, LVL Living sought to collect the full amount of rent that would have been due through the end of the lease—regardless of whether the unit was re-rented.

The legal question is: can a landlord accelerate the remaining rent on the lease term under F.S. 83.595?

F.S. § 83.595 is the statute that governs the landlord’s remedy options in the event the tenant terminates the lease early. One of the remedy options requires that landlords mitigate damages by attempting to re-rent the unit and crediting the prior tenant for any replacement rent received if the landlord chooses that remedy option under. Under that same statute, landlords also have the option to “sit back and do nothing” and charge the tenant rent for the remaining term of the lease if the landlord does not retake possession of the unit. See our articles on the landlord’s remedy options here, here, and here.

The Plaintiffs argue that LVL Living unlawfully accelerated the remaining eight months of rent following their eviction, in violation of both F.S. 83.595 and the lease agreement itself. They assert that the lease—drafted by the Defendants—expressly incorporated the statutory requirements of F.S. 83.595, which they argue prohibits blanket rent acceleration and requires landlords to mitigate damages by re-renting the unit and only collecting rent as it accrues. Plaintiffs contend that LVL ignored these requirements by preemptively charging the full remaining lease balance, despite knowing the unit was re-rented by the end of May 2024.

Under Florida law, the obligation to pay future rent ceases once the unit is relet. Therefore, Plaintiffs claim they were only responsible for accrued rent between January and May 2024. By demanding the full lease balance and sending it to collections even after the unit was re-rented, Plaintiffs allege that LVL Living engaged in unlawful debt collection practices, violating both the Florida Residential Landlord and Tenant Act (FRLTA) and the Florida Consumer Collection Practices Act (FCCPA).

Florida courts have held that a landlord cannot simultaneously retake possession of a rental unit and claim entitlement to the full balance of rent under an acceleration clause. A 2025 Florida case addressed this issue. Here is what the court ruled,

“A landlord can resume possession of the premises by either accepting tenant’s surrender or by obtaining a writ of possession. See § 83.595, Fla. Stat. However, where the landlord resumes possession-regardless of whether it is for its own account or on behalf of the tenant-it cannot simultaneously claim it has chosen to “stand by and do nothing”:

‘Either of the first two [remedies] excludes the third. By retaking possession either for his own account or for the account of the lessee, a lessor loses the right to recover the full amount of remaining rental due on the basis of an acceleration clause. The two positions are inconsistent (emphasis added).’”

Hefley v. Holmquist, 5D2021-1378 (Fla. App. Feb 06, 2025), citing DeLoach, 362 So.2d at 984 (citing Geiger Mut. Agency, 233 So.2d 444; Jimmy Hall’s Morningside, 235 So.2d 344).

At the outset of this case, the landlord may have a problem with the issue of rent acceleration and debt collection fees on that amount, if it is shown that the landlord retook possession and re-rented the premises. In that situation, the landlord could very well be incorrect in demanding $17,032.00 and the debt collection fee of 40% of that amount ($6,812.80), thus reducing the debt balance demand by $23,844.80.

Landlord Tip: Be Cautious When Accelerating Rent

Landlords should not attempt to accelerate the full balance of rent due under a residential lease or send to collections unless three key conditions are met—keeping in mind that the results of the LVL Living case on this issue could impact future landlord practices:

- The lease expressly provides for rent acceleration in the event of tenant default;

- The landlord has not retaken possession of the property (either by accepting surrender or obtaining a writ of possession); and

- If the landlord decides to take possession and re-rent the unit, the landlord should clearly communicate this to the tenant, apply any rent collected from a new tenant during the remaining lease term to the tenant’s account, and treat any debt collection attempts accordingly.

Failing to meet these requirements risks violating F.S. 83.595 and could expose the landlord to legal claims for unlawful debt collection or improper lease enforcement.

40% Collection Fee

Another central issue in the lawsuit is LVL Living’s imposition of a 40% debt collection fee, which was added to the Plaintiffs’ account balance when their alleged debt was referred to a third-party debt collection company. The Plaintiffs contend that this fee was not authorized by the lease agreement, not supported by Florida law, and grossly inflated the amount they were told they owed—raising the balance from approximately $25,000 to over $34,000.

According to the complaint, this charge was automatically added without any showing that the collection agency had performed substantial services or that the fee reflected actual costs incurred. Plaintiffs argue that the 40% fee constituted an unlawful and deceptive debt collection practice, further compounding the stress and financial burden they faced.

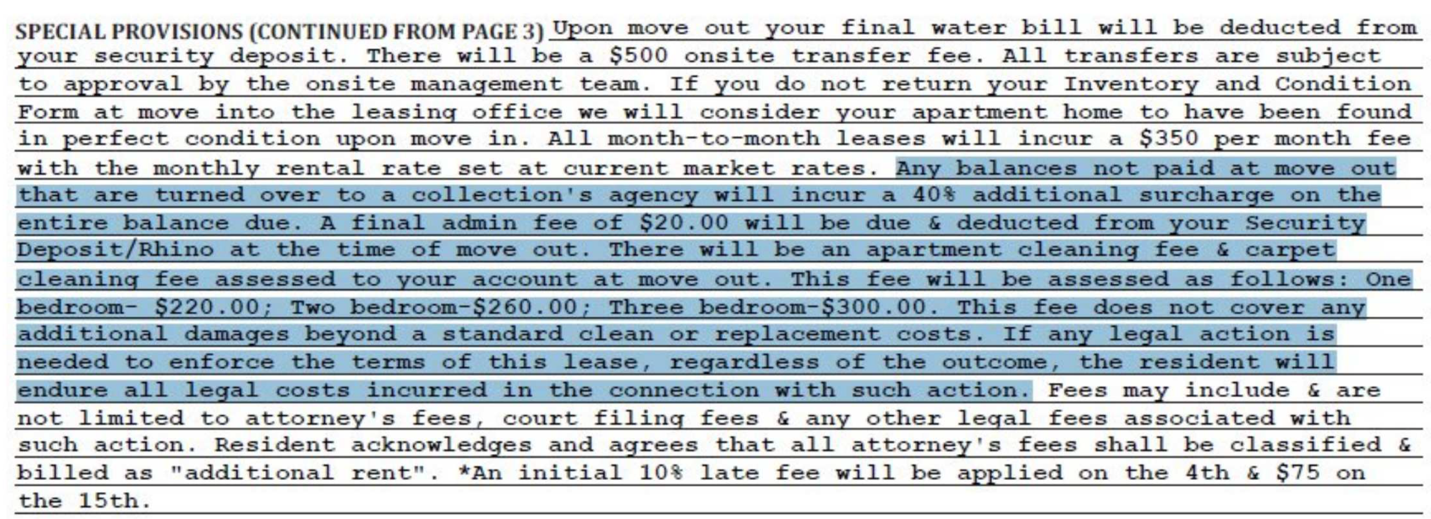

The lease, “Special Provision”, does provide for a 40% debt collection fee. It states,

The Plaintiffs, however, alleges that they did not agree to this provision. The Complaint states,

“The above provision appears on page 10 of the 57-page Lease. The provision is not actually in the actual lease itself, nor is it in any addendum. Rather, it appears alone, on its own page, after the Parties signed on the lease.”

On this basis, the Plaintiff alleges that they never agreed to the 40% debt collection fee. Whether the Plaintiff agreed to this provision or not, of course, may have a significant impact on the result of the landlord’s charge of the debt collection fee.

If the judge or jury finds that the Plaintiff did, in fact, agree to this provision, the question turns to, is this provision enforceable or unenforceable as a matter of law (and as to the other issues raised by the Plaintiff), which is yet to be seen in this case.

Landlord Tip: Avoid Prematurely Sending Balances to Collections

When pursuing unpaid rent or damages, landlords should avoid sending tenant balances to collections prematurely, especially when the amounts are based on future rent. Here are two key safeguards:

Do not send accelerated rent balances to collections until the lease term has ended—this ensures that the total amount actually owed can be accurately calculated, especially after accounting for any rent collected from a new tenant.

Alternatively, if not accelerating rent, only send balances for rent that has already accrued, not for future months, to comply with F.S. § 83.595 and avoid potential violations of Florida law.

Sending inflated or speculative balances to collections may expose landlords to legal liability for attempting to collect an unlawful debt.

How FL Landlords Can Avoid Similar Lawsuits

While this case has just begun, the LVL Living class action lawsuit serves as a critical reminder that aggressive post-tenancy billing practices—such as automatic rent acceleration and large debt collection fees—can carry significant legal risk when not carefully aligned with Florida law and the terms of the lease. Whether or not LVL Living ultimately prevails in this litigation, the case highlights common pitfalls that landlords must avoid to remain compliant with Florida law. Landlords should ensure that any financial claims made after a tenant vacates are based on clearly written lease provisions, reflect actual accrued damages, are properly documented, and comply with legal requirements. Equally important, landlords must avoid prematurely sending speculative or inflated debts to collections, as doing so may expose them to liability for various consumer and debt collection protections in Florida. As this case unfolds, it may establish new precedent and guidance for the rental housing industry—not just in Florida, but across the country.